Stock Market Outlook

For The Week Of August 11th =

Downtrend

INDICATORS

-

ADX Directional Indicators: Downtrend

Price & Volume Action: Downtrend

On Balance Volume Indicator: Mixed

The stock market outlook enters the second week of a downtrend after an extremely volatile week for global equity traders.

Despite all the price movement, the S&P500 ($SPX) was flat for the week. The index sits ~2% below the 50-day moving average and ~6% above the 200-day moving average.

SPX Technical Analysis - August 11 2024

The ADX and institutional activity remain bearish. On Balance Volume shifts to mixed as it oscillates around its moving average.

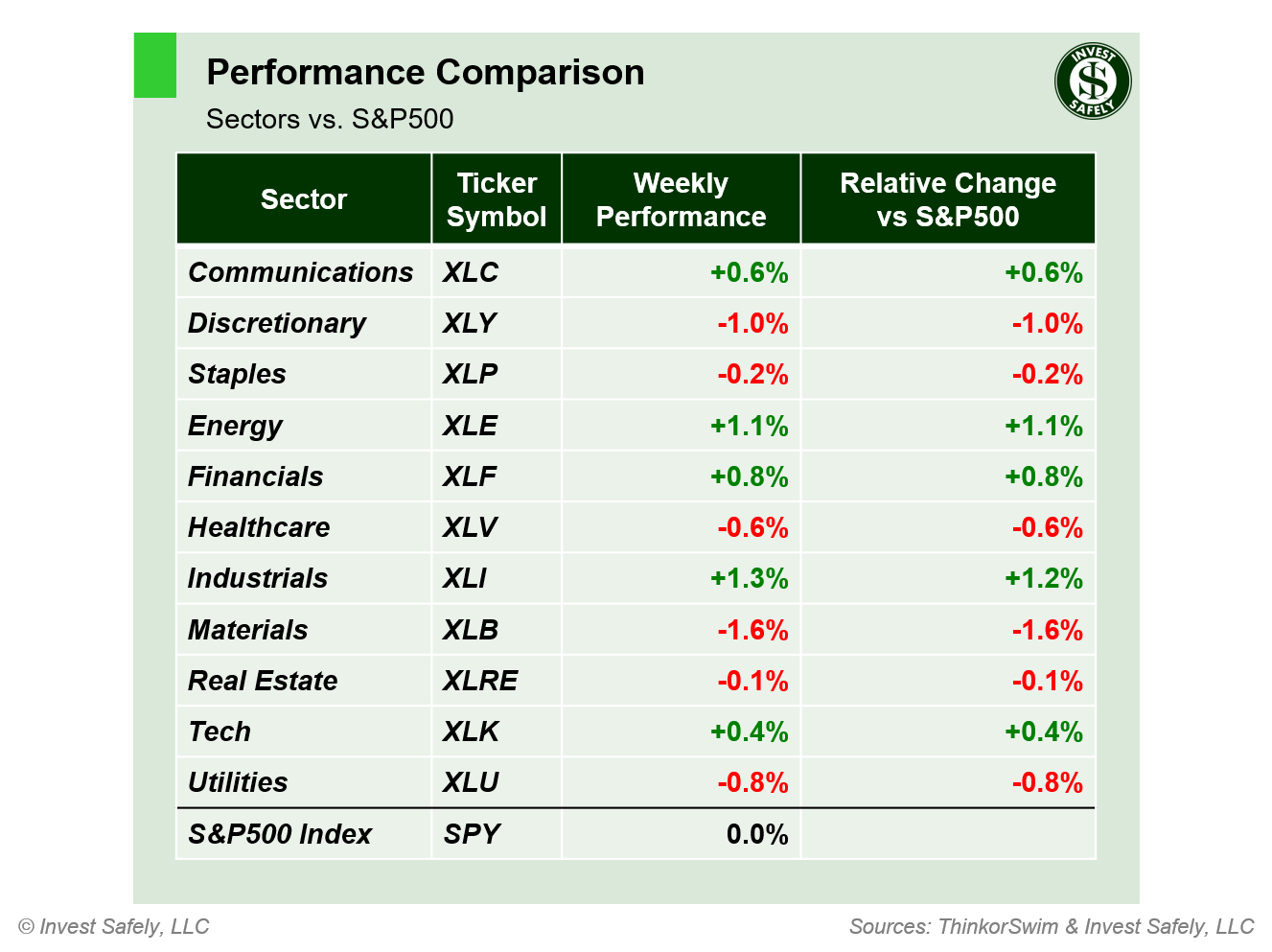

Sector-wise, Industrials were the best performer last week ($XLI), while Materials ($XLB) led to the downside (an odd pairing for best/worst sectors).

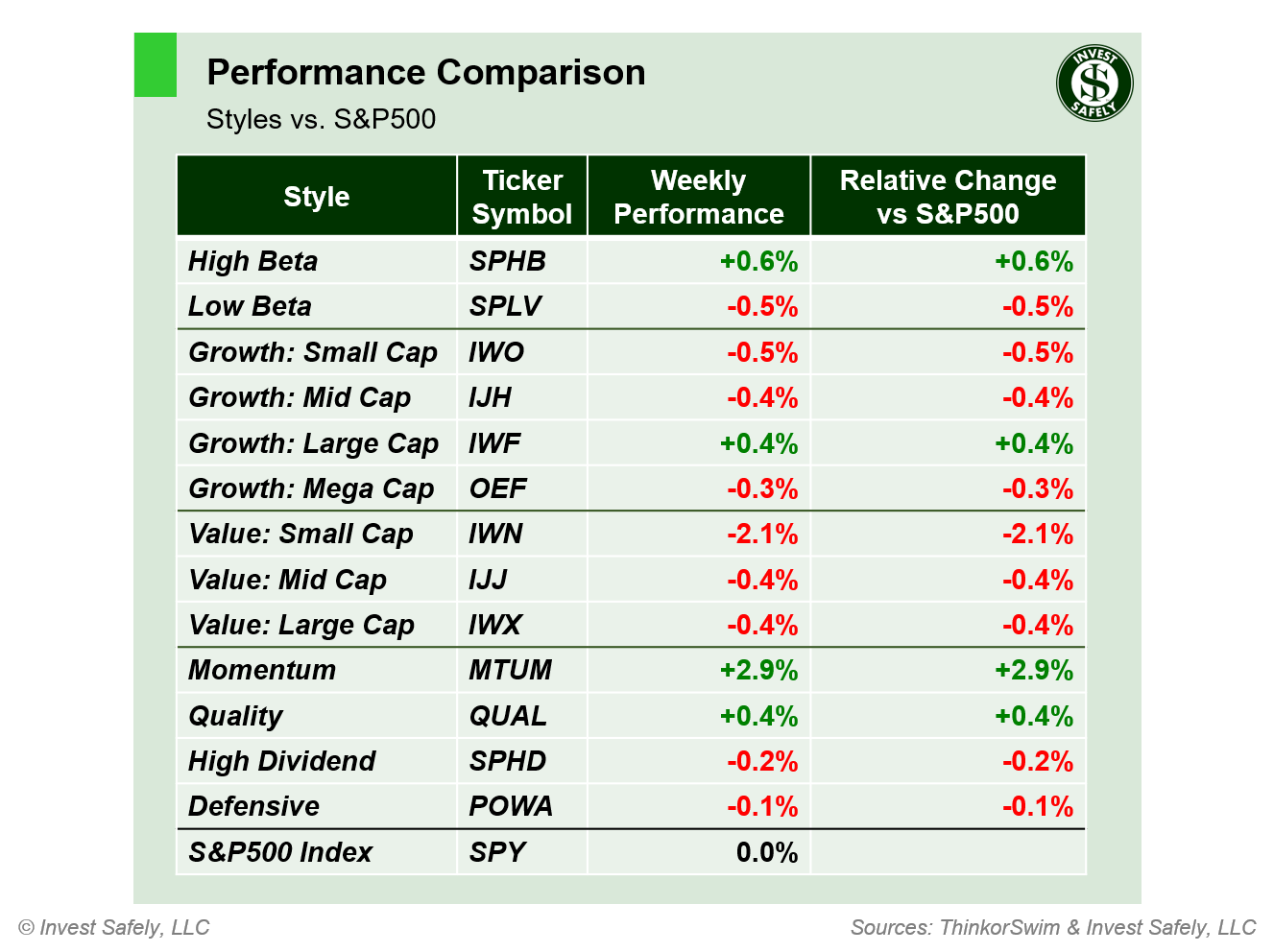

From a sector style perspective, Momentum was the best, while Small Cap Value was the worst. Both were at extremes (oversold/overbought, respectively), so the reversions aren't too surprising.

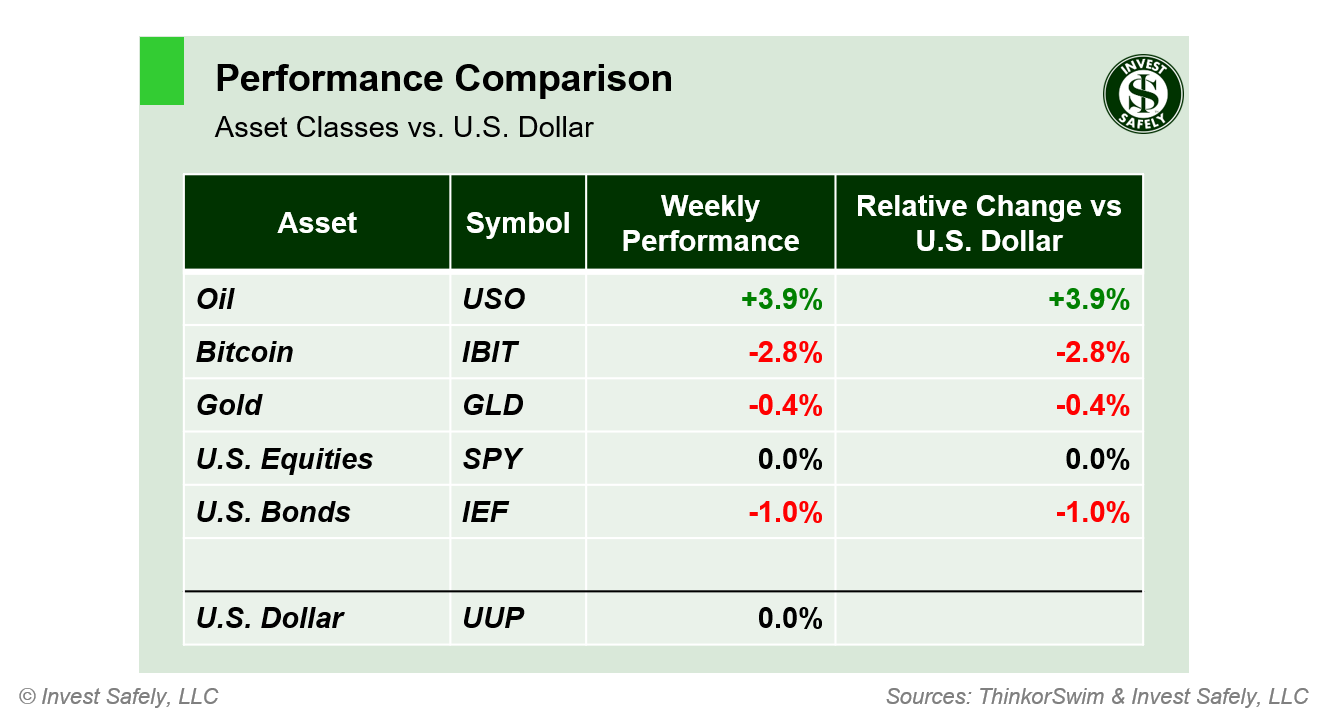

Bitcoin led to the downside again last week, but by a much smaller margin than last time. Oil led the way higher.

COMMENTARY

Last post, the Sahm rule and recession fears that were top of mind for financial media. Last week, it was the Yen-Carry trade crashing global markets, and the need for the U.S. Fed to provide emergency rate cuts.

The Bank of Japan announced a rate hike, which caught market participants off guard and sent the Nikkei index down more than 12% in one day. Japanese stocks recovered a majority of those losses in the following session.

Policy surprises of any kind tend to generate volatility, which is why the Fed has started putting the word out months ahead of any policy change (remember when the FOMC was thinking about "thinking about" rate hikes a few years ago?).

The resulting equity market volatility stoked fears that the long-awaited unwind of the Yen-carry trade was in progress. We discussed the Yen carry trade back in March when the first hike was announced.

In the States, some pundits initially attributed the U.S. sell-off to the lower than expected jobs data, released the prior Friday. The knee-jerk reaction was a call for emergency rate cuts to stave off the further weakening of the stock market...I mean the economy...I mean price stability and labor markets<wink>.

It doesn't matter that the same outlets were dismissing the idea of any economic or labor weakness when the GDP figures were released two weeks ago. Newsflash: the Fed isn't supposed to prop up equity markets (whether they do from time to time, in coordination with the Treasury, is another discussion entirely).

As equity markets recovered, financial media softened their call for immediate rate cuts. The creator of the Sahm rule was trotted out on several networks to cool recession fears, stating that this time really is different because immigration, specifically unemployed immigrants, is skewing the number higher.

By the end of the week, the narrative had settled on knee-jerk reactions to the surprise jobs data and BOJ rate hike. Maybe they all realized that an emergency rate cut would create even more pressure to unwind the yen-carry trade, not to mention signaling a lack of confidence in the current market environment, both of which could provide another downside catalyst. Or maybe too much money was allocated to low volatility trading strategies and got caught offsides...

Regardless of the narrative, volatility returned in a BIG way last week, with the SPX volatility index ($VIX) reaching the mid-60's on Monday. As a reminder, a reading above 30 is considered an extremely difficult time to hold equities due to big, fast price swings. It's also when equities tend to underperform other asset classes.

Sure enough, recent asset class and sector price movement also align with a weaker environment for equities, with leadership in Bonds & Gold / REITs & Utilities indicating a deflationary environment in place (when measuring their relative performance over the past 4 weeks).

More volatility could be in the cards this week, with the release of the latest inflation data (PPI & CPI). The year over year comparisons aren't particularly high, so we should see inflation flat or slowing, bolstering the calls for rate cuts in September.

Best to Your Week!

P.S. If you find this research helpful, please tell a friend.

If you don't, tell an enemy.

Sources: Bloomberg, CNBC, Federal Reserve Bank of St. Louis, Hedgeye, U.S. Bureau of Economic Analysis, U.S. Bureau of Labor Statistics

Share this Post on:

How to Make Money in Stocks: A Winning System in Good Times and Bad.

It's one of my favorites.

I regularly share articles and other news of interest on:

Twitter (@investsafely)

Facebook (@InvestSafely)

LinkedIn (@Invest-Safely)

Instagram (@investsafely)

Invest Safely, LLC is an independent investment research and online financial media company. Use of Invest Safely, LLC and any other products available through invest-safely.com is subject to our Terms of Service and Privacy Policy. Not a recommendation to buy or sell any security.

Charts provided courtesy of stockcharts.com.

For historical Elliott Wave commentary and analysis, go to ELLIOTT WAVE lives on by Tony Caldaro. Current counts can be found at: Pretzel Logic, and 12345ABCDEWXYZ

Once a year, I review the market outlook signals as if they were a mechanical trading system, while pointing out issues and making adjustments. The goal is to give you to give you an example of how to analyze and continuously improve your own systems.

- 2015 Performance - Stock Market Outlook

- 2016 Performance - Stock Market Outlook

- 2017 Performance - Stock Market Outlook

- 2018 Performance - Stock Market Outlook

- 2019 Performance - Stock Market Outlook

- 2020 Performance - Stock Market Outlook

IMPORTANT DISCLOSURE INFORMATION

This material is for general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purpose. Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. Invest Safely, LLC is not a law firm, certified public accounting firm, or registered investment advisor and no portion of its content should be construed as legal, accounting, or investment advice.

The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this website does not constitute a representation that the investments described herein are suitable or appropriate for any person.

Hypothetical Presentations:

Any referenced performance is “as calculated” using the referenced funds and has not been independently verified. This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any reader or contributor, from any specific funds or securities.

The author and/or any reader may have experienced materially different performance based upon various factors during the corresponding time periods. To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including:

Model results do not reflect the results of actual trading using assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight

Back-tested performance may not reflect the impact that any material market or economic factors might have had on the use of a trading model if the model had been used during the period to actually manage assets

Actual investment results during the corresponding time periods may have been materially different from those portrayed in the model

Past performance may not be indicative of future results. Therefore, no one should assume that future performance will be profitable, or equal to any corresponding historical index.

The S&P 500 Composite Total Return Index (the "S&P") is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor's chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet investment objective(s). The model and indices performance results do not reflect the impact of taxes.

Investing involves risk (even the “safe” kind)! Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of underlying risk. Therefore, do not assume that future performance of any specific investment or investment strategy be suitable for your portfolio or individual situation, will be profitable, equal any historical performance level(s), or prove successful (including the investments and/or investment strategies describe on this site).

Investing Process Links

Stabilize- Organize your $$$

- Manage your $$$

Plan

- Why You Invest

- Ways to Invest

- Where to Invest

- What to Invest In

Execute

- When to Invest

- How Much to Invest

- Buying & Selling

Monitor

- Track The Market

- Track Your Returns

Reflect & Adjust

- Improve Your Returns

- Adjust your Holdings

Popular Pages

- Jim Cramer- Personal Incomes Statements

- Hyperinflation

- Calculating Beta

- SMART Financial Goals

Blogroll

- Advisor Perspectives- Dividend Growth Investor

- Elliott Wave Lives On

- On My Radar | CMG Wealth

- Sure Dividend

- The Big Picture

- The Fat Pitch

- Thoughts from the Frontline

- Trader Feed

Sponsored Links

Invest Safely provides valuable, time-saving info about personal finance, money management, and investing.